🙋🏻♂️ A Short Preface

Hello there, glad you’re interested in the 8th edition of Deep Tech Demystified! This is kind of a special post, as this time I won’t dive into a specific technology, but rather in a type of business model within Deep Tech: full-stack Deep Tech, or vertically integrated Deep Tech - call it what you will. In short: sell “whole products” instead of being a parts/service supplier. Given the (AI) technology cycles we’re currently in, the geopolitical tensions that are omnipresent and an increasing focus on national interests in Europe, this business model is more relevant than ever. If you then look at the track record of companies that embraced this form of company building, it only comes natural to feel the urge to immerse oneself in this part of Deep Tech. That’s why I’m also keen on finding ‘the one’ this year, that goes full-stack. If you’re building a full-stack hardware company, please reach out to felix@playfair.vc!

🇪🇺 The ‘European’ Deep Tech Approach

Before we dive into what full-stack encompasses and why I’m such a fan of that model, let me quickly tell you about the constantly reoccurring pattern that I’ve witnessed in four years of startup operations and venture in Europe within the tech domain.

I’ve dubbed this the ‘European’ approach, but this certainly happens all over the globe. From what I’ve personally seen, more and more ambitious founders in Europe arise that cast aside this pattern and go full-stack. But it is with most things in life: the more the merrier. Hence why I’m writing this one.

Teams usually find an industry that is ready to be disrupted by a new technological trend or is posed to benefit tremendously from the adoption of said technology. The “European” approach is most of the time the following: build something software- and/or hardware-enabled that fits into the complex supply chain or behavioural patterns of the incumbents. Then prototypes will get trialed and iterated with the big brand names. Oftentimes, this is mistaken for commercial validation - commercially valid to an incumbent maybe, but not venture scale valid. On the back of that, the teams raise a few millions of (pre-)Seed money. Because being a (sub-) contractor to corporates is not too ambitious or crazy, investors feel very comfortable and are happy to invest. The cooperations with corporates will be broadened, commercial contracts will be set in place and more often than not, the teams will pull together a Series A - oftentimes even with support from the incumbents. And then the fun begins. Incumbents do what they are good at - protecting the status quo. Building some real traction becomes more and more challenging as you have to fight your way through corporate culture, an unwillingness to change and iterate rapidly. Suddenly, your Series A company is mainly constrained by sales cycles and decision processes of publicly listed corporates - which are limited in count and thus, you have no alternative but to submit to them. On top of that, your value creation potential is inherently capped by the corporate’s value creation potential. Congratulations, your startup just transformed into an extension of [insert whatever big corporate comes to mind].

Approaches like these sound very reasonable in a growth capital-constrained venture ecosystem in Europe, especially with dried up exit markets and strategic acquisitions being one of the few exit routes remaining at the moment. That’s why so many founders and VC’s alike like these models. The problem is though, that they are rarely successful in the context of venture outcomes - hence why we need full-stack Deep Tech to radically rethink entire industries and eventually, become the entire industry ourselves. Ambitious, but that is what venture should all be about!

🏭 Why Full-Stack Deep Tech?

Now that we have set the stage, let’s dive into what being a full-stack Deep Tech company actually means. The short summary the following: instead of building a product to sell into an industry, which as a consequence can build and sell a complete product to customers, just build the whole thing yourself and become the industry - ideally in a monopolistic setting. In that way, you can bypass all the existing companies struggling to catch the next technology wave. All the while reaping all the benefits of owning the entire supply- and value creation chain. The more detailed reasoning below as taken from Ian Rountree’s “Full-Stack Deep Tech”, Chris Dixon’s “The Full-Stack Startup” as well as Packy McCormick’s Vertical Integrator Series with my perspective added on top. Please note that the benefits of a full-stack concept also hold true to most parts for companies producing for commodity markets - like chemicals - because producing and selling commodities is very similar to producing and selling whole products.

Control & Speed: A full-stack approach provides more control over the rate of the company’s growth, bypassing slow incumbents. Unlike companies that rely on external sales cycles and might even get hindered by cultural resistance within corporates, full-stack companies are limited primarily by their funding. The latter is one of the reasons this model becomes so challenging in Europe and always relies on relocating the company to the US, or bringing in foreign investment. Overall, not that great for Europe, but still great for (pre-) Seed and A investors.

Customer Diversity: Selling a “whole product” usually leads to a broadened customer base and less dependence on a few large partners - which are typically slow incumbents. This gives you not only independence in terms of partnerships to choose from, but also reduces the risk associated with losing a major customer or partner. On top of that, you have the luxury to sell your customer what they actually want and not something they need to get what they want. This is a small nuance, but makes sales so much easier and faster.

Product Progression & Optionality: Full-stack companies can more easily expand into new product lines, respectively building on top of their existing offering. From a (pre-) Seed perspective, this is incredibly challenging, given that most likely you’ll start with only an idea or maybe an industry and it’ll be hard to predict the longterm future and how industries mature. But it is pretty much a given, that once you’re an integral part of an industry you’ll build on top of your foundation. Think of Apple and their expansion from iMac, to iPod, iPhone, iPad and the Apple Watch.

Economic Upside: Full-stack companies often have a much larger potential market compared to component or equipment sellers. While the full-stack approach will definitely squeeze the achievable gross margins compared to a supplier setup, the overall market size and potential is typically larger. This is also in part due to the above mentioned point and the convenient way in which you can systematically expand you TAM. Another facet of this is a monopoly on customer data, which allows for products on top of products.

Customer Experience: Full-stack companies have complete control over the product experience from end-to-end. This can result in a better, more seamless product for customers and can even be a longterm point of differentiation. Again, Apple is a wonderful example, where complete control over their product ecosystem shapes a unique customer experience. Compare this to the “modularity” of Microsoft building parts of the product and relying on partners to assemble a whole product.

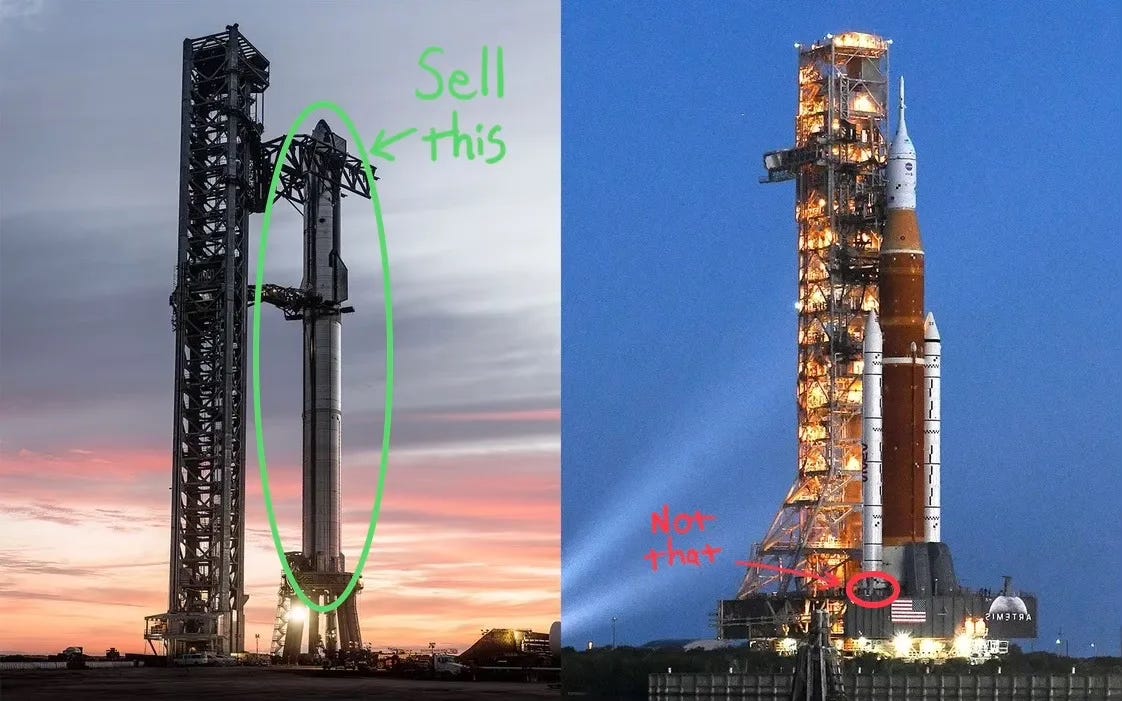

Capital Efficiency: This one seems counterintuitive at first but actually makes a lot of sense if you think of it from a longterm perspective. The initial stages of a full-stack Deep Tech venture will be more capital intensive, because of the full-stack approach and also because Deep Tech is initially eating up more capital. But in the long run, capital efficiency will rule, given that once an industry is unlocked, this also means that you can yield higher margins, on a foundation (ideally) run with a ‘capital-constrained-mindset’ in contrast to a ‘bureaucratic-incumbent-mindset’. If this happens in the context of a monopoly and you’re a price setter even better. The key from an early stage perspective is though, to find companies that need a relatively low amount of CAPEX/OPEX spending to reach commercialisation stage - full-stack is no excuse for huge infrastructure investments! In the example of SpaceX, they’ve reached that first stage after $90M of funding - quite little money to get a huge rocket into space if you ask me.

Entry Barriers: Given the complex nature of full-stack companies, with many interconnected pieces, competitors will struggle to replicate them and grab market shares in the short- and mid-term. Incumbents that need to pivot will struggle, because that means cannibalising themselves on a large scale. Also, more often than not, the combination part is one of the key value drivers of full-stack companies, which will make it incredibly difficult for others outside of the industry to enter. If you sprinkle some resource constraints on top of that, you might even have a total disruption of existing industries with nearly no way to catch-up again - looking at you BYD and my dear German automotive industry.

⏳ When Full-Stack Deep Tech?

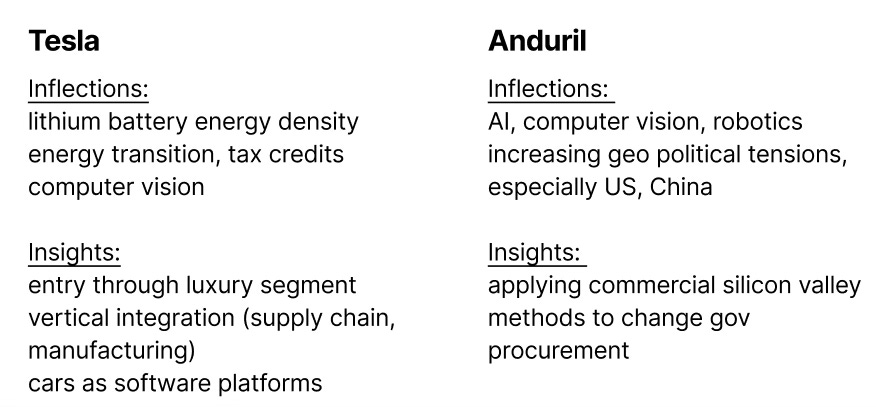

As with nearly everything in life, timing is key. To be real though, I don’t think there are major differences to full-stack Deep Tech investing compared to “traditional” Deep Tech investing, looking at it purely from a technology angle. As stated in the intro of this article about the “European” approach, most founders even look for the right signs as to when an industry is ripe for the next technological wave. The major difference I would argue is though, that you have to look out and account for inflection points that happen beyond technology in, for example, culture and geopolitics. Below you can see exemplary inflection points that defined the right timing for Tesla building full-stack EVs and Anduril building full-stack autonomous defence systems. If you want to read more on “the anatomy of inflections,” take a look at this wonderful essay from Alexander Lange.

To be able to put all these different shifts together and to form a clear picture about how the future might look like is incredibly challenging and also very risky, especially at an early stage. Would you have been able to spot the early signs for SpaceX in 2002? Maybe, but maybe you would have been busy watching Lord of the Rings - The Two Towers, that just came into cinema a few months before their first institutional round. Feel old yet?

To be fair, The Two Towers is a great piece of cinema and if you truly missed investing in SpaceX because you were busy watching the scene “Battle of Helm’s Deep” over and over again like I did, you are excused - absolute class.

To get back to business again, what I want to say with this is, the signs are out there years before most are able to pick them up. And in that sense, a lot of investors (and founders) overly fixate on the future, while the actual challenge lies within clearly seeing the present and dismantling the inflections happening right now. Alexander Lange’s essay gives you two powerful concepts to get better at this: contextual awareness - to see inflections in the context of their present circumstances and why they are inflections at this particular point in time; and time resolution - considering the time horizon in which these inflections occur, because they will happen across unique timescales. Seriously, check his essay out!

But there is also another way of thinking, that might help you get a clearer picture to see when full-stack Deep Tech might make sense:

Value in Rebuilding Old Systems: A lot of industries build up some form of technical debt. Technical debt in this context means, that mature industries accept one technology layer as de-facto standard and pretty much build whole organisations on top of it. At the time of emergence this is definitely reasonable, but longterm, novel technology layers might be more appropriate. Think for example of Microsoft Excel that is still used in a lot of industrial settings as data storage. If this debt accumulates over multiple layers - which happens more often than not in monopolistic or oligopolistic industries - there might be actual value in completely rethinking how these industries are run and organisations assembled. Simply switching out a single layer with a novel one won’t work in most cases, as these layers will be surrounded by more technical debt and the overall outcome will still be limited by the weakest link. And without external shocks in form of, for example, new entrants or drastic geopolitical shifts, the existing industry players have little incentive to restructure their technical debt. Industries that come to mind are automotive, manufacturing and commercial aerospace.

📜 My Thesis

As stated in the intro, I really want to find ‘the one’ this year - in Europe. Not a small feat, but everyone can use a bit of professional growth! What I look out for is simple:

Zero Market Risk: I firmly believe that the purpose of a Deep Tech venture should be really simple, because the process of building is already complex enough. This means, if your team can overcome all the technical challenges, people will go out of their way to buy your product. If there are huge philosophical debates around why this product might be useful to some people at some point in time, I won’t invest. Sounds lazy at first, but simply means if I’m taking on a huge upfront risk of full-stack & Deep Tech at pre-Seed, the outcome potential must be a given. Market pivoting is simply too expensive, given the huge sunk cost.

Team Execution Speed & Scrappiness: There is a simple difference between SpaceX and Blue Origin. Each of them are funded respectively by pretty much the biggest entrepreneurs of our time, but one launches scrappy prototypes and the other falls more into the “German engineering” (sorry fellow Germans) category, seeing value in perfection. You can guess which one has been more successful at launching mass into space (and bringing it safely back to earth) - hint: it’s not Blue Origin. Building something full-stack means being able to see the bigger picture, constantly and repeatedly and to act accordingly.